J.P. MORGAN ASSET MANAGEMENT - Millennials: Navigating conversations with the next generation of wealth

Generational differences can present a challenge when navigating money management. Discover the best practices for making these conversations more fruitful.

"Should the traditional asset management industry hope to best serve this group, successfully navigating both early conversations and ongoing relationships will be a key differentiator."

Data recently released by the Census Bureau show that the age distribution of the U.S. population has shifted in the last 10 years: the bloc of Americans aged 30-39 grew by over 4% between 2010 and 2020, and of the top 10 ages by frequency, not one is above the age of 35. This is the rise of the “Millennial.”

This rise has been reflected in soaring home prices and broader spending data (Millennials and their younger counterparts, Gen-Z, account for roughly a third of U.S. credit card spend)1. This trend looks set to continue: Millennials are poised to inherit roughly $68 trillion from their parents by 20302. The net result of this generational shift is that money management conversations are changing, with the asset management industry paying closer attention to younger Americans.

However, generational differences and, in some cases, a distrust of the financial services industry stemming from coming of age during the GFC, can make navigating these conversations a challenge. Below are series of “best practices” that can make these conversations more fruitful:

- Communication preferences: “digital first” – but not “digital only”

“Cold calls” on the phone are unwelcome, and communication preferences tend to skew digital for first contact, either with a text message or an email; however, most social media is to be avoided, the result of a clear delineation between “professional” and “personal” channels. These texts or emails should be brief and to the point, but can result in a more in-depth conversations, either over the phone, virtually or in person.

- Experiences are valued and “perks” are welcomed.

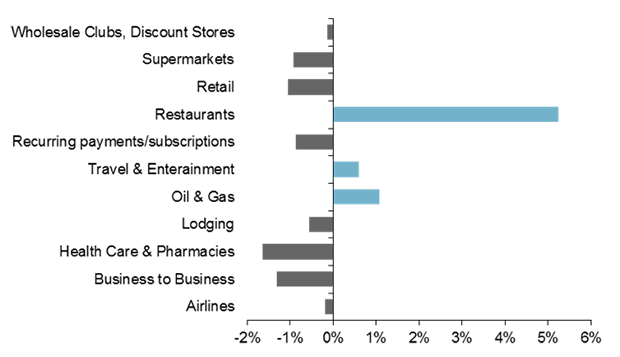

Younger Americans tend to gravitate more toward experiences rather than goods: according to credit card spending data, Millennials and Gen-Z spend more on restaurants, travel and entertainment, and less on retail and supermarkets, than older cohorts. Moreover, membership “perks” – like those associated with a high-end credit card – are welcomed, especially since cash flow can be constrained at younger ages. These two things suggest a heightened interest in advisor-sponsored events, especially in a post-COVID world where many are eager to socialize.

- Being proactive is key, but beware the risk of oversaturation.

Young professionals are busy; many are eager to distinguish themselves in their careers with long hours, and even those that aren’t can feel constantly on call, particularly now that working from home has been proven viable. For an advisor, being proactive can be helpful, but there’s a fine line between helpful, actionable insights and what some may consider spam. Communications should be infrequent and punchy – like a newsletter with “best ideas” or thought leadership on current market and macro conditions.

As Millennials and Gen-Z grow wealthier, so too will their financial needs grow more complex.

The role of financial advice will, as a result, become of paramount importance. Should the traditional asset management industry hope to best serve this group, successfully navigating both early conversations and ongoing relationships will be a key differentiator.

Millennials and Gen Z spend less on goods, more on experiences

Generational differences in credit card spend, 5/31/19 - 3/1/20

Source: J.P. Morgan Asset Management, based on internal Chase data. Data as of March 31, 2020.

Consumers continue to rate ‘high quality’ and ‘good value for money’ as the most important factors in their decisions. This is backed up by our engagements with fashion companies, who claim that consumers are not willing to pay a premium for sustainability, although at the same price point they would choose the more sustainable offering.

To us, this signals that consumers have a preference for sustainability and it can be a competitive advantage for retailers. But companies need to see it as a way to maintain or grow their market share rather than a way to increase prices. Sustainable leaders should be investing in innovation and scale for sustainable solutions to bring prices down and maintain their brand position.

1 Chase credit card spending data, May 2019 – March 2020.

2 Coldwell Banker, A Look at Wealth 2019: Millennial Millionaires.

Important Information:

This communication has been prepared exclusively for institutional, wholesale, professional clients and qualified investors only, as defined by local laws and regulations. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction, nor is it a commitment from J.P. Morgan Asset Management or any of its subsidiaries to participate in any of the transactions mentioned herein. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, based on certain assumptions and current market conditions and are subject to change without prior notice. All information presented herein is considered to be accurate at the time of production. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any securities or products. In addition, users should make an independent assessment of the legal, regulatory, tax, credit and accounting implications and determine, together with their own financial professional, if any investment mentioned herein is believed to be appropriate to their personal goals. Investors should ensure that they obtain all available relevant information before making any investment. It should be noted that investment involves risks, the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Both past performance and yield are not a reliable indicator of current and future results.