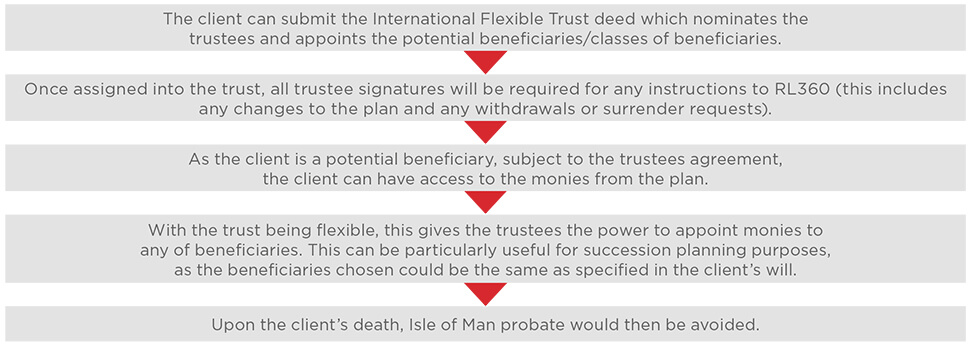

International Flexible Trust

The RL360 International Flexible Trust is designed to assist non-UK long term resident plan owners with their succession planning objectives.

Issues for consideration

- The trust is not suitable for someone who is, or could become UK long term resident, as the trust has a wide class of beneficiaries (of which the Settlor is one) and it would therefore be a Gift with Reservation. It would also form part of the client’s estate for UK inheritance tax purposes.

- The International Flexible Trust can be used with a new application for an RL360 plan, or with an existing RL360 plan. However, this cannot be used where the existing plan is owned by a company or a trust.

- If it is decided at a later date that client no longer wishes to have the plan in the trust, then the trustees can assign the ownership of the plan back to the client.

- After the death of the client, if there are surviving lives assured, or the plan is written on a capital redemption basis, the trustees can assign the ownership of the plan or plan segments to a beneficiary aged 18 or over

Important notes

Please note that every care has been taken to ensure that the information provided is correct and in accordance with our current understanding of the UK law and HM Revenue and Customs (HMRC) practice as at April 2025. You should note however, that we cannot take on the role of an individual taxation adviser and independent confirmation should be obtained before acting or refraining from acting upon the information given. The law and HMRC practice are subject to change.