Loan Trust

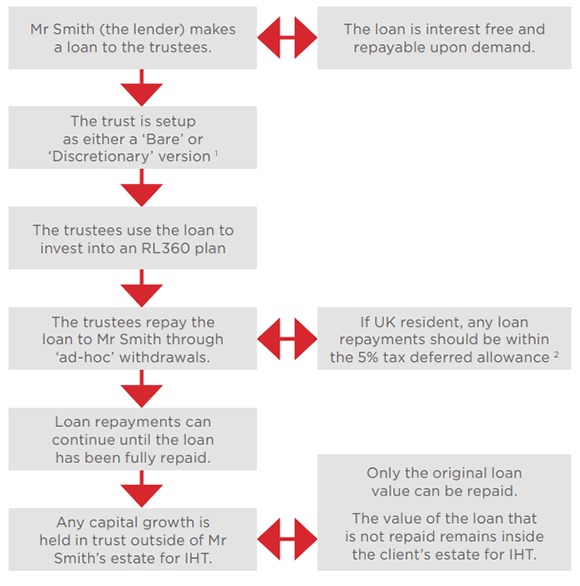

The RL360 Loan Trust allows an individual to make a loan into a trust, rather than an outright gift. Learn more about the UK Inheritance Tax (IHT) benefits of the Loan Trust in the following document and by reading our separate Guide to Trusts.

How does it work?

Issues for consideration

- The Loan Trust is only available for use with new applications. It cannot be setup on an existing plan.

- The lender can request the loan to be repaid at any time.

- Only the outstanding loan amount can be repaid to the lender.

- There are no restrictions on the amount or frequency of repayments.

- Taking more than 5% of the cumulative tax deferred allowance as a withdrawal in a plan year could trigger a chargeable event if UK resident.

- Only the growth is outside of the settlor’s estate for IHT planning.

- Any loan repayments that have not been spent will remain inside of the estate.

1 The loan is neither a chargeable lifetime transfer (CLT) nor a potentially exempt transfer (PET). Therefore, it remains inside the estate even after 7 years.

2 If the lender is a UK resident, any repayment of the loan outside of the 5% tax deferred cumulative allowance may be treated as a chargeable event.

Client scenario

In this case study, Mr Smith would like to carry out UK Inheritance Tax (IHT) planning, but is not willing to give up access to his capital.

The problem

His total wealth of £650,000 exceeds the current nil?rate band (NRB) (£325,000 for 2019/2020). He is concerned about any potential IHT charge that might befall his estate on death. If he were to die today, there would be a potential IHT liability of £130,000.

The IHT liability is calculated as follows:

- £650,000 less £325,000 (NRB allowance) = £325,000

- £325,000 x 40% (current IHT tax charge) = £130,000

Mr Smith would like a way to retain access to the capital to meet future expenditure needs. At the same time would like to ensure that his family don’t pay more IHT than required.

The RL360 Loan Trust solution

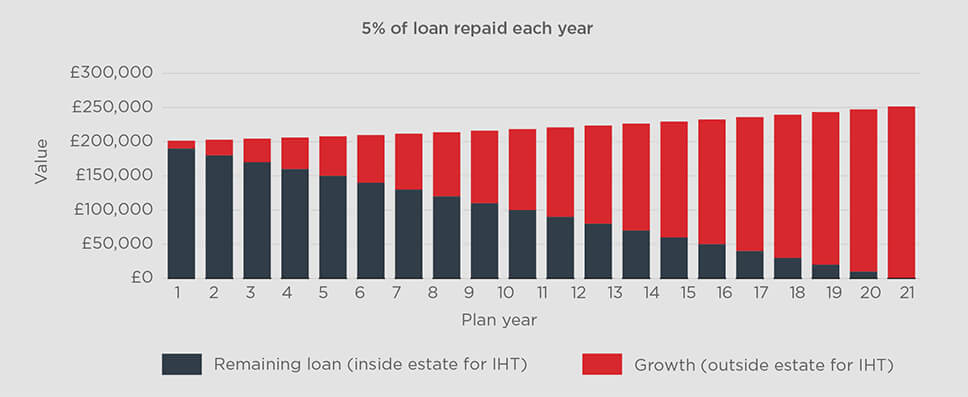

Mr Smith, (the lender), makes an interest free loan of £200,000 to the trustees. The trustees use the loan to invest the capital into an RL360 plan. Mr Smith requests that the trustees make a repayment of £10,000³ each year to supplement his income.

Any amount of the loan that has not been repaid remains inside Mr Smith’s estate for IHT. However, any growth on the investment is immediately outside of his estate for IHT.

As illustrated in the chart below, by plan year 21 the whole loan of £200,000 has now been repaid.

Assuming the investment grows at approx. 6% per annum after fees, the growth (approx. £251,000) is outside of Mr Smith’s estate for IHT.

Providing that Mr Smith has been spending any loan repayments that have been received the IHT liability should have been reduced.

IHT calculation

The IHT liability is calculated as follows:

- £650,000 less £200,000 (value of loan now repaid and spent) = £450,000

- £450,000 less £325,000 (NRB allowance) = £125,000

- £125,000 x 40% (current IHT tax charge) = £50,000

By using the Loan Trust, it has reduced the potential IHT liability by £80,000 (£200,000 * 40%).

Important notes

Whilst this document highlights the opportunity for planning, it is not intended to provide an exhaustive analysis of all the opportunities or pitfalls. Please note that every care has been taken to ensure that the information provided is correct and in accordance with our current understanding of the UK law and HM Revenue and Customs (HMRC) practice as at April 2025. You should note however, that we cannot take on the role of an individual taxation adviser and independent confirmation should be obtained before acting or refraining from acting upon the information given. The law and HMRC practice are subject to change.

³ This represents 5% of the loan (£200,000). For a UK resident, the 5% tax deferred accumulative amount is the maximum that can be withdrawn each plan year without triggering a chargeable event.