BlackRock - 2023 Global Investment Outlook

A new investment playbook

The regime of greater economic and market volatility is playing out – and not going away. Central banks won’t ride to the rescue in recession, contrary to what investors have come to expect. This regime requires a new investment playbook. It involves more frequent portfolio changes and more granular views that go beyond broad asset classes.

Investment Themes

01. Pricing the damage

Central banks are deliberately causing recession by overtightening policy to tame inflation, in our view. That makes recession foretold. What matters: our view on the pricing of economic damage and our assessment of market risk sentiment. Investment implication: We stay underweight DM equities but expect to turn more positive at some point in 2023.

02. Rethinking bonds

We see higher yields as a gift to investors long starved of income in bonds. And investors don’t have to go far up the fixed income risk spectrum to receive it. Investment implication: We like short-term government bonds, investment grade credit and agency mortgage-backed securities for income. We stay underweight long-term government bonds.

03. Living with the inflation

Long-term trends of the new regime, such as aging workforces and geopolitical fragmentation, will keep inflation persistently above pre-pandemic levels, in our view. Investment implications: We stay overweight inflation-linked bonds on both tactical and strategic horizons. We are strategically overweight DM equities.

Global Investment Outlook

New regime playing out

The Great Moderation, the four-decade period of largely stable activity and inflation, is behind us. The new regime of greater economic and market volatility is playing out – and not going away, in our view. Central banks are deliberately causing recessions by overtightening policy to try to rein in inflation. That makes recession foretold.

We see central banks eventually backing off from rate hikes as the economic damage becomes clear. We expect inflation to cool but stay persistently higher than central bank targets of 2%. Repeated inflation surprises have sent bond yields soaring, crushing equities and fixed income. Such volatility stands in sharp contrast to the Great Moderation era.

A key feature of the new regime, we believe, is that we are in a world shaped by production constraints. The pandemic shift in consumer spending from services to goods caused shortages and bottlenecks. Aging populations led to worker shortages. This means DMs can’t produce as much as before without creating inflation pressure. That’s why inflation is so high now, even though activity is below its pre-Covid trend.

A brutal trade-off

Central bank policy rates are not the tool to resolve production constraints; they can only influence demand in their economies. That leaves them with a brutal trade-off.

Either get inflation back to 2% targets by crushing demand down to what the economy can comfortably produce now, or live with more inflation. For now, they’re all in on the first option. So recession is foretold. Signs of a slowdown are emerging. But as the damage becomes real, we believe they’ll stop their hikes even though inflation won’t be on track to get all the way down to 2%.

Production constraints

Some production constraints could ease as spending normalizes. We see three long-term trends keeping production capacity constrained and cementing the new regime:

1. Aging populations mean continued worker shortages in many major economies.

2. Persistent geopolitical tensions are rewiring globalization and supply chains.

3. The transition to net-zero carbon emissions is causing energy supply and demand mismatches.

What’s clear to us is that what worked in the past won’t work now.

Our new playbook

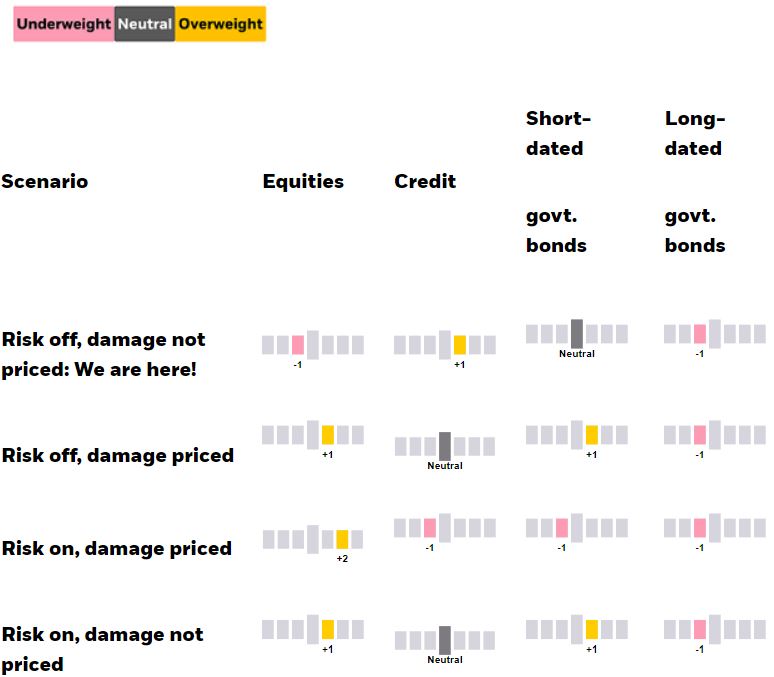

Navigating markets in 2023 will require more frequent portfolio changes and a new investment playbook. It also calls for taking more granular views by focusing on sectors, regions and sub-asset classes, rather than on broad exposures. What matters most for our tactical portfolio outcomes, we think, are two assessments: 1) our assessment of market risk sentiment, and; 2) our view of how much economic damage is already reflected in market pricing.

The table above shows how we plan to change our views as markets play out in the new regime. A few key conclusions:

- We are already at our most defensive stance. Other options are about turning more positive, especially on equities.

- We are underweight nominal long-term government bonds in each scenario in this new regime. This is our strongest conviction in any scenario.

- We can turn positive in different ways: either via our assessment of market risk sentiment or our view on how much damage is in the price.

Important Information:

Capital at Risk

All financial investments involve an element of risk. Therefore, the value of the investment and the income from it will vary and the initial investment amount cannot be guaranteed.

Past performance is not a reliable indicator of current or future results. It is not possible to invest directly in an index. Sources: Blackrock Investment Institute, November 2022. Notes: The boxes in this stylized matrix show how our tactical views on broad assets classes would switch if we were to change our assessment of market risk sentiment or assessment of how much economic damage is priced in. The potential view changes are from a U.S. dollar perspective. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast or guarantee of future results. This information should not be relied upon as investment advice regarding any particular fund, strategy or security.

December 2022

Please note that these are the views of BlackRock Investment Institute Team and should not be interpreted as the views of RL360.