Fidelity - Why equity investors are rediscovering Japan

Most global investors remain unappreciative and under-allocated when it comes to Japanese stocks. But this risks missing out on the quiet but steady transformation that’s unfolding in Japan amid striking improvements in corporate earnings yields and capital returns.

What is it about Japanese stocks that has “confounded” Warren Buffett, ultimately convincing him to make Japan his second-biggest equity allocation globally, after the United States?

The answer is no secret but still may come as a surprise to many. In short, Japan has - steadily and quietly - spent the past few years transforming itself into one of the most attractive markets anywhere in terms of improving earnings yields and capital returns. Just don’t tell that to global investors (or even local investors) - most of whom remain chronically under-allocated to Japanese stocks.

After all, Japan is already the second-biggest country weight in most global equity benchmarks. As investors realise what’s on offer, we think there are several reasons why that gap in allocations may be set to narrow. A major shift has played out in Japan over the past decade, and the drivers for it are many: regulatory reforms, corporate innovation, a stronger economy, and a bigger focus on capital efficiency. But it all adds up to a better landscape for investors.

Follow the money

Consider shareholder returns. In a recent interview with CNBC, Buffett said that what drew him to put billions to work in Japanese stocks was the fact he could invest at double-digit earnings yields and still hope to see his dividend payments grow substantially over time. “It’s turned out to be better than I thought it would be,” he said.

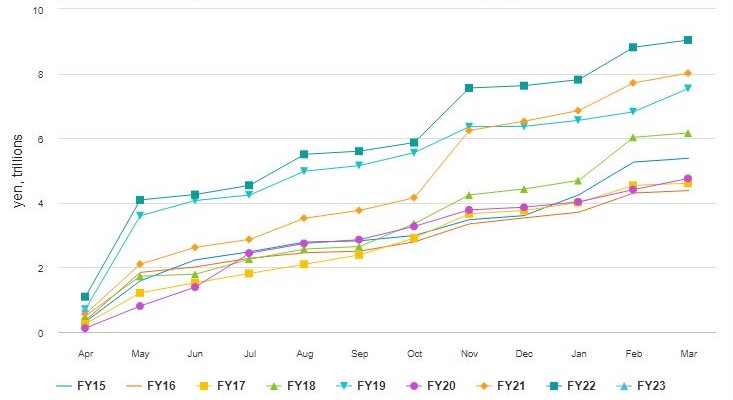

Chart 1: Share buybacks in Japan hit a record last year

Monthly share buyback plan announcements by fiscal year (FY), cumulative

Note: Data covers TOPIX constituents. Source: Nikkei QUICK, SMBC Nikko, Fidelity International, May 2023

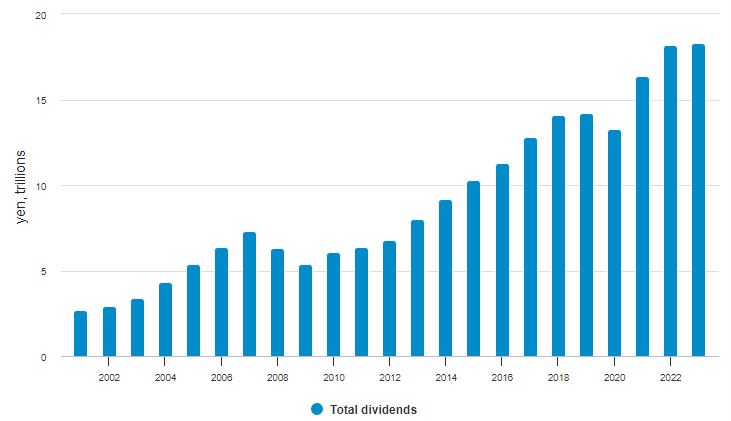

It’s not difficult to see how Japan might surprise on the upside. Japanese companies have acquired huge cash piles over the years and sat on them, and have come under criticism for inefficient capital allocation as a result. But that characterisation of Japan Inc looks increasingly outdated: in recent years Japanese companies have been returning more capital to shareholders than ever. In the fiscal year just ended, TOPIX companies carried out record levels of share buybacks, while at the same time paying out the biggest amount of total dividends to date. At the same time, shares in Japanese companies continue to look attractively priced on a relative valuation basis, especially when compared with valuations on US equity benchmarks, for example.

A new era of reform?

Those changes are being driven in part by top-down regulatory overhauls intended to boost capital efficiency in Japan’s stock market. The Tokyo Stock Exchange (TSE) last year restructured the market into three segments, with higher governance standards for the newly formed Prime segment, where nearly half of TSE stocks are currently traded. For example, one new push with direct implications for shareholder returns is that Prime segment companies are being subjected to more scrutiny over their capital efficiency, especially at firms that are trading below book value, and are being asked to “properly identify” their cost and efficiency of capital.

Chart 2: Japanese companies are paying out more dividends than ever

Note: Data covers TOPIX constituents. Source: Nikkei QUICK, SMBC Nikko, Fidelity International, May 2023

While these measures are encouraging, we think it’s even more important to introduce incentives for companies to pursue sustainable growth. More can be done. For example, the new governance requirements in the Prime segment employ a “comply or explain” principle. In practice, there is little consequence for companies that skip past “comply” and go directly to “explain”, treating it as a formality. Stricter enforcement is needed. In a similar vein, we see value in revamping the methodology for compiling the TOPIX. Currently, the index automatically absorbs Japanese stocks when they get listed, in contrast to global benchmarks like the S&P 500, which have a cap on the number of constituents.

More can and will be done but the progress that’s been made on the regulatory reform front is already delivering tangible results for Japan’s markets and investors. That includes further measures improving governance, like bringing down cross-shareholdings. These were a common trait of traditional Japanese corporate management a generation ago, whereby the boards of cross-held companies seek to maximise their control by leveraging their combined voting power to support each other. Such structures often run contrary to the interests of independent shareholders, and they can also frustrate outside attempts to bring change or consolidation to underperforming companies. While cross-shareholdings are on the wane, it’s still true today that the longer a company’s tenure as a member of the TOPIX, the more likely it is to have more of its equity tied up in such structures. Removing cross shareholdings can only help to improve the overall competitiveness of Japanese corporates, paving the way for more mergers and acquisitions, facilitating consolidation within certain sectors, and promoting better returns on capital across the market.

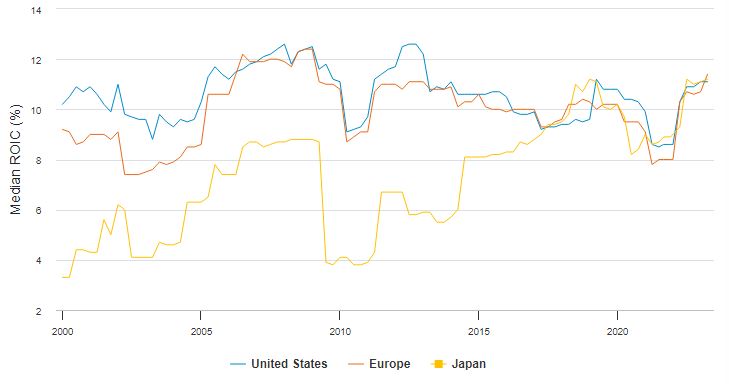

Chart 3: Japanese companies have made structural improvements to how they deploy capital in their businesses

Median returns on invested capital (ROIC) by MSCI region

Source: Jefferies, Factset, Fidelity International. Data as of March 31, 2023

Macro challenges, innovative solutions

This year, neighboring China’s massive population declined for the first time in a half a century, the clearest evidence yet that the world’s second largest economy is following Japan (the third largest) down a demographic path that leads to a rapidly aging society and shrinking workforce. But the lessons from Japan in terms of economic output or corporate performance are that growth and innovation can not only be sustained but accelerate against such a backdrop.

Indeed, Japan has long since shaken off the drag from the “lost decades” that held its economy hostage in a deflationary spiral through most of the 1990s and 2000s. A turning point came in 2012 with the launch of then Prime Minister Shinzo Abe’s package of economic and financial market reforms, known as ‘Abenomics’. The decade since has been better characterised by steady and stable growth, whether that’s measured by overall output, capital expenditure or total wages. As a result, Japan Inc’s earnings have outgrown the developed world, with expanding margins a significant driver of this. While a weaker currency has also been a factor in this relative outperformance, business reform and cost-cutting have also clearly contributed.

Chart 4: Earnings growth in Japan has outstripped the rest if the world

12 month forward earnings per share (EPS) for major world stock indices

Note: Local currency returns rebased to 100 as at 31 Dec, 2011. TOPIX for Japan, S&P 500 for US, DJ Stoxx 600 for Europe, MSCI Asia Pacific ex Japan Index for APxJ, MSCI AC World Index for World.

Source: Refinitive Datastream, Fidelity International, data through 30 April, 2023.

Japan has also largely dodged the inflationary bullet that’s torn through many Western economies and caused headaches for their central bankers amid the last few years of pandemic-induced price surges and other disruptions. By contrast, Japan is one place where a little inflation is generally welcomed. While some worry about the prospect of inflation running away, the moderate price increases Japan is seeing so far act as an anti-deflationary buffer. It can also serve as a cyclical boon to the economy, as companies start to increase wages at meaningful levels that policymakers hope will stimulate more consumer spending as a result.

Many of those companies are globally competitive industry leaders and innovators, which have the pricing power to absorb those cost increases and still grow profits. Those include software and IT services firms that are helping Japanese companies to overcome labour shortages and raise productivity, while made-in-Japan and designed-in-Japan factory automation solutions are being exported globally. Healthcare innovators add to the dynamism while growth in dividends continues to gain momentum across many Japanese corporates.

Finally, Japan is a quiet leader in the region and globally when it comes to prioritising environmental, social and governance (ESG) factors. Overhauls at the stock exchange come alongside revisions to the corporate governance code that have helped make shareholders’ concerns more of a priority for managements. What’s more, Japanese financials and corporates are emerging as global leaders in the drive to net zero. Japan is home to more institutions supporting the Task Force on Climate-related Financial Disclosures (TCFD) than any other market globally.

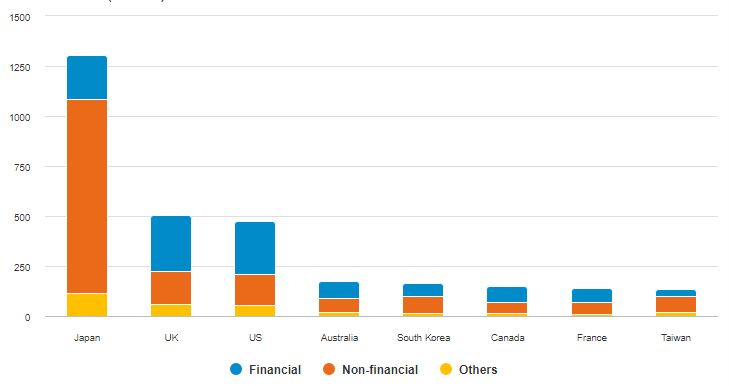

Chart 5: Japanese companies are embracing the drive to ‘net zero’

Number of institutions supporting the Task Force on Climate-related Financial Disclosures (TCFD)

Source: TCFD consortium, data as of 24 April, 2023

Under-owned for how long?

Despite the improved outlook of recent years, investors - both foreign and local - haven’t kept pace in terms of their allocations. Global active funds remain net underweight Japan (although less underweight than they were, say, 2-3 years ago when Covid broke out). And Japanese households too are relatively underweight equities when it comes to their mix of financial assets, as compared against their counterparts in the US or Europe.

These structural underweights suggest there is ample room for inflows to Japan’s markets. If the corporate sector, guided by even more shareholder-friendly policymaking, can continue to build on its success in recent years in boosting returns, Warren Buffett won’t be the only one buying.

Important Information

This document is for Investment Professionals only and should not be relied on by private investors.

This document is provided for information purposes only and is intended only for the person or entity to which it is sent. It must not be reproduced or circulated to any other party without prior permission of Fidelity.

This document does not constitute a distribution, an offer or solicitation to engage the investment management services of Fidelity, or an offer to buy or sell or the solicitation of any offer to buy or sell any securities in any jurisdiction or country where such distribution or offer is not authorised or would be contrary to local laws or regulations. Fidelity makes no representations that the contents are appropriate for use in all locations or that the transactions or services discussed are available or appropriate for sale or use in all jurisdictions or countries or by all investors or counterparties.

This communication is not directed at, and must not be acted on by persons inside the United States and is otherwise only directed at persons residing in jurisdictions where the relevant funds are authorised for distribution or where no such authorisation is required. Fidelity is not authorised to manage or distribute investment funds or products in, or to provide investment management or advisory services to persons resident in, mainland China. All persons and entities accessing the information do so on their own initiative and are responsible for compliance with applicable local laws and regulations and should consult their professional advisers.

May 2023

Please note that these are the views of Fidelity International and should not be interpreted as the views of RL360.