GAM - Locking Opportunities in Emerging Markets

Emerging market equities offer compelling opportunities, but demand selectivity. Investment Director Ygal Sebban highlights targeted areas of strength, driven by structural trends, policy support and valuation appeal.

Successful emerging markets (EM) investing requires a deep understanding of global macroeconomic (macro) trends, including trade flows, geopolitical shifts and structural challenges in developed markets (DM). Capital flows and risk sentiment in EMs are often shaped by DM dynamics, making a top-down, risk-aware approach essential.

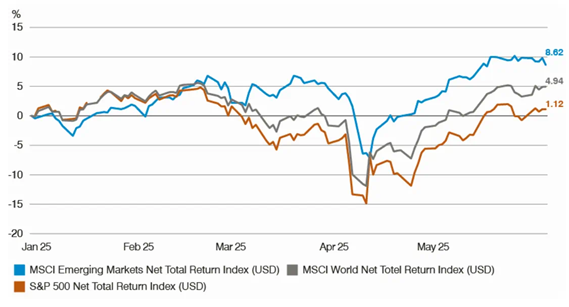

Chart 1: Year-to-date (YTD) performance of EM versus MSCI World and S&P 500

Source: Bloomberg, as at 30 May 2025.

Past performance is not an indicator of future performance and current or future trends.

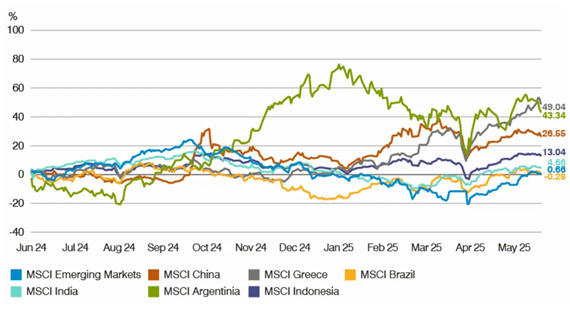

Chart 2: Divergence in EM performance

One-year performance from 31 May 2024 to 30 May 2025

Source: Bloomberg, as at 30 May 2025.

Past performance is not an indicator of future performance and current or future trends. Note: All are Net Total Return indices in USD.

EMs have had a strong run this year, outperforming global markets. The MSCI Emerging Markets Index (USD) has returned 8.62% YTD, outpacing both the MSCI World Index’s 4.94% and the S&P 500’s 1.12% (all in USD, as at 30 May 2025). This outperformance highlights the importance of selectivity and active management in capturing the right opportunities.

The performance dispersion across EM markets underscores the importance of active management. Markets within the EM universe do not move in unison; each responds differently to macroeconomic forces, political developments and structural shifts. This divergence creates both opportunities and risks that passive strategies may overlook.

We assess EMs based on relative attractiveness, evaluating risk-adjusted valuations, growth prospects, momentum and quality. Key return drivers, such as currency, GDP growth, political stability and exposure to global themes like artificial intelligence (AI) and the energy transition, are evaluated using proprietary models that incorporate real interest rate differentials, volatility and balance of payments.

Current market focus: China, Greece and Argentina

We are currently focusing on three markets: China, Greece and Argentina. While Greece and Argentina are quite insulated from the trade war, our positioning in China emphasises themes that are also resilient to such risks.

China remains a core focus, supported by a shift towards more pro-growth policies, reaffirmed in recent government meetings. The 5% growth target for 20251 signals continued stimulus. We are particularly constructive on the software and consumer discretionary sectors, favouring service consumption over goods, particularly travel, local service platforms, AI and gaming. These areas benefit from attractive valuations, improving earnings momentum and dual policy tailwinds: “Digital China” and the push for “home-grown” technology. Companies like Kingdee and Kingsoft have delivered strong earnings surprises2,3, driven by operational leverage and cost discipline.

Greece stands out for its strong risk-adjusted return profile following its upgrade to investment grade status. We anticipate above-consensus GDP growth of 2.5% in 2025, supported by prudent fiscal policy and structural reforms. Persistent primary surpluses should drive a steady reduction. We are positive on Greek banks, where capital return potential, including share buybacks, is increasingly compelling.

Argentina is also a focus, reflecting a macro recovery story. Since December 2023 the country has implemented bold reforms in deregulation, privatisation and fiscal discipline. A successful tax amnesty has attracted USD 22 billion in inflows, while annual inflation has dropped sharply, from 211% at the end of 2023 to 47% in April 20254. Headline inflation is projected to continue its downward trajectory, reaching 37% in 2025 and 15% in 20265, supported by monetary tightening and currency reform. With private credit expanding from a low base, and banks are expected to play a key role in Argentina’s recovery, we see significant upside in the banking sector, an opportunity we believe is not yet fully priced in.

These markets offer compelling opportunities supported by favourable macro trends, reform momentum and positive earnings outlooks.

China: still investable

We continue to see selective opportunities in China, particularly in areas supported by structural trends and proactive policy. The macro environment has shifted meaningfully, with the government prioritising growth and private sector confidence over the earlier focus on “common prosperity”.

Since September 2024, China has demonstrated coordinated support across monetary, fiscal, housing and capital market policies. Liquidity conditions have improved, and we see signs of housing market stabilisation, which could help lift broader sentiment – even if a return to pre-Covid activity levels remains unlikely.

We are constructive on China’s outlook, driven by a reaffirmed 5% GDP growth target for 2025, a more accommodative policy mix, including a 4% fiscal deficit, and targeted support for consumption, property, banking and capital markets. Recent policy meetings continue to signal that further stimulus is on the table.

Our focus is on software and consumer discretionary sectors, where we see attractive risk-adjusted returns. In consumer discretionary, we favour service-led areas such as travel, local platforms, AI and gaming, trading at the lower end of their five-year valuation ranges with improving earnings momentum. Recent results from leading internet and e-commerce firms have exceeded expectations, driven by strong operational leverage and product innovation.

In software, China's advanced AI capabilities, exemplified by DeepSeek, and national strategies like “Digital China” and technology localisation continue to support growth. While we remain mindful of geopolitical risks and tariffs, which may impact exporters, we avoid the most exposed areas and focus on themes less vulnerable to external shocks.

Tariffs and EM: risks and responses

Despite several alterations to the US tariffs, such as temporary reductions and tech exemptions, and signs of negotiation between China and the US, international trade remains under pressure. Tariff rates are significantly higher than anticipated as the start of the year, weighing on international trade, business confidence, and ultimately global growth. Yet, we believe the secular trends in EMs remain intact, offering resilience in a shifting landscape.

While tariffs do present challenges for EMs, the impact varies by country, and several countries have demonstrated the ability to respond effectively. While tariffs can disrupt trade flows, pressure exporters and increase input costs, their severity largely depends on each country's economic structure and sector exposure. We view the direct impact of tariffs as more pronounced on the economies imposing them, such as the US, than on EMs broadly. Most EMs do not import significant consumer goods from the US, so inflationary effects tend to be limited. Instead, the main consequence is pressure on EM exporters to the US, a risk we actively manage by avoid companies and sectors most exposed to these risks.

That said, EMs are not uniformly vulnerable. Economies driven by domestic demand, like India and Brazil, are more insulated than export-reliant peers such as Mexico or Vietnam. China, for example, has responded with targeted stimulus, tax relief and accelerated its transition towards higher-value sectors such as software and AI, areas benefiting from policy support and localisation trends.

More broadly, tariffs are accelerating the divergence between EM and DM growth trajectories – often to the benefit of EMs. By encouraging self-sufficiency and regional trade, they are reinforcing structural shifts already underway in many EMs. For investors, this creates new opportunities in markets focused on innovation, domestic growth and policy-driven resilience.

A weaker US dollar: What it means for EMs

A weaker US dollar has historically supported EM returns, with the two showing a strong inverse relationship. This dynamic benefits EM assets through three primary channels:

Capital flows: A depreciating US dollar attracts foreign capital inflows, as investors seek higher returns, which in turn supports corporate earnings and economic expansion.

Debt servicing: A softer dollar reduces the burden of dollar-denominated debt for EM sovereigns and corporates.

Commodities: Commodity prices are crucial, as many EMs are commodity exporters. Commodity prices tend to rise when the US dollar weakens, offering a further boost to economic performance.

Additionally, a weaker dollar gives EM central banks greater policy flexibility, allowing them to ease monetary conditions or hold rates. In contrast, a stronger dollar often forces EMs to tighten policy defensively, as was seen in 2018.

Looking ahead, we anticipate further US dollar depreciation, supported by fiscal stimulus and inflation expectations. Structural factors, such as concerns over US fiscal sustainability and undervalued EM currencies, should also provide medium-term tailwinds for EM currency.

Positioning for what’s next

EMs continue to offer compelling opportunities for investors who can navigate their complexity with discipline and insight. While global headwinds such as tariffs and geopolitical tensions persist, many EMs are demonstrating resilience through structural reforms, domestic demand, and alignment with transformative global trends like AI and energy transition. A weaker US dollar further enhances the outlook, supporting capital flows, easing debt burdens, and boosting commodity-linked economies.

By combining top-down macro analysis with bottom-up stock selection, and focusing on policy-supported, innovation-led sectors, we aim to identify the most attractive opportunities while actively managing risk. In our view, the evolving EM landscape is not only investable, it is increasingly an essential component of a forward-looking global portfolio.

Important legal information

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not a reliable indicator of future results or current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented and are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. There is no guarantee that forecasts will be realised.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in indices which do not reflect the deduction of the investment manager’s fees or other trading expenses. Such indices are provided for illustrative purposes only. Indices are unmanaged and do not incur management fees, transaction costs or other expenses associated with an investment strategy. Therefore, comparisons to indices have limitations. There can be no assurance that a portfolio will match or outperform any particular index or benchmark.

The foregoing views contains forward-looking statements relating to the objectives, opportunities, and the future performance of the markets generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of GAM or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

June 2025

Please note that these are the views of Ygal Sebban of GAM Investment and should not be interpreted as the views of RL360.