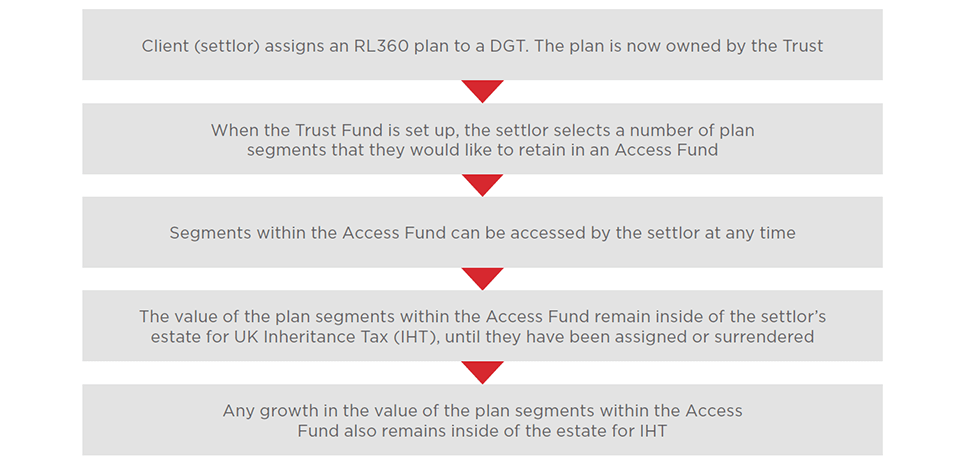

Discounted Gift Trust (Access Fund)

The Access Fund is an additional feature of the DGT that allows plan segments to be held separately from the remaining part of the Gifted Fund. These plan segments can be accessed by the settlor at any time.

The addition of an Access Fund allows flexibility over a normal DGT. Plan segments can be surrendered if additional income is required, or even gifted to a new owner by assignment.

The DGT Access Fund process

A DGT with an Access Fund follows the same principles as a DGT without an Access Fund:

- The value of withdrawals (The Discount) under DGT is based on the underwriting decision

- The Discount is deducted from the transfer value into the DGT to give a Discounted Value

- Only the Discounted Value and NOT the actual value of transfer when plan assigned into DGT are included in the estate for IHT should death occur in first 7 years

- After 7 years the Discounted Value is outside of estate for IHT

- Any growth – excluding the Access Fund - is immediately outside of the estate for IHT

Example

The problem

Mr Smith (aged 62) is aware of the benefits of using the DGT for reducing his IHT liability. However, he is unsure of his future spending requirements and would like to retain access to some of the capital.

The RL360 DGT solution

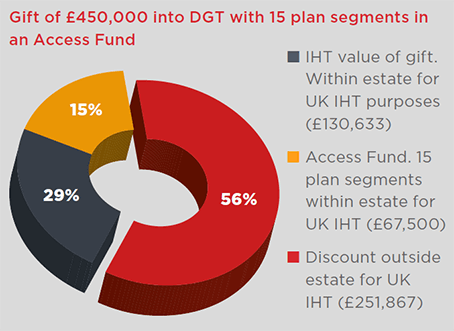

He makes an investment of £450,000 into an RL360 plan issued with 100 segments. The plan is gifted to the DGT. Each plan segment is valued at £4,500 (£450,000/100).

85 plan segments (£382,500 (£450,000/100 x 85)) are allocated to the Gifted Fund, and 15 plan segments (£67,500 (£450,000/100 x 15)) are retained in the Access Fund.

He decides to carve out an immediate yearly income of £22,500* (£450,000 x 5%) payable on a monthly basis.

* 5% is selected to ensure withdrawals are kept within the cumulative 5% allowance for UK chargeable event purposes.

For a plan with an Access Fund the discount is only calculated on the amount that was placed into the Gifted Fund: £382,500 (£450,000 - £67,500).

In accordance with HMRC guidance, the withdrawals to be paid to the settlor in his lifetime are valued at £251,867** and therefore the value of their gift is discounted to £130,633 (£382,500 - £251,867).

The discounted value of £130,633 (plus the value of the Access Fund)will be the amount that is declared for UK IHT should Mr Smith die within 7 years of making the gift.

After 7 years, the remaining £130,633 will then be outside of their estate for IHT purposes.

The value of the plan segments retained in the Access Fund remain inside of the estate even after 7 years.

The growth of the Gifted Fund is immediately outside of their estate for IHT purposes. (This excludes the Access Fund).

* £19,125 comes from the Gifted Fund and £3,375 from the Access Fund.

** The discount is immediately outside of the estate for IHT

Using the Access Fund

Mr Smith has decided that he would like to help his adult grandchild with their house purchase by making a gift of £21,000. Mr Smith is allowed to do this even if the grandchild is not included as one of the trust beneficiaries.

The Trust Fund is currently £525,000; each of the 100 plan segments is now valued at £5,250 (£525,000/100). 15 plan segments were retained in the Access Fund. The current value of the Access Fund is £78,750 (£5,250 x 15).

To achieve the gift of £21,000 he has the following options:

- Surrender 4 plan segments (£5,250 x 4) and make a gift to the grandchild. Any tax liability for any chargeable gains would fall on Mr Smith, or

- Assign 4 plan segments (£5,250 x 4) to their grandchild. The grandchild could then surrender the plan segments in their own name. The tax liability for any chargeable gain would then fall on the grandchild.

It is not possible to take a withdrawal solely from the Access Fund.

Once plan segments within the Access Fund have been gifted or surrendered, the settlor's regular withdrawal payments will also decrease.

Example:

If the total annual income when trust is first setup = £22,500, made up of £19,125 (retained rights) from the Gifted Fund and £3,375 from the Access Fund, as Access Fund segments are gifted or surrendered, the value of withdrawals from the Access Fund will decrease from £3,375 down to £0. The settlor’s income from the Gifted Fund income remains unchanged throughout their lifetime (or until such time as the trust fund is exhausted).

Important notes

For financial advisers only. Not to be distributed to, nor relied on by, retail clients. Whilst these case studies highlight the opportunities for planning, they are not intended to provide an exhaustive analysis of all the opportunities or pitfalls. Please note that every care has been taken to ensure that the information provided is correct and in accordance with our current understanding of the UK law and HMRC practice as at April 2025. You should note however, that we cannot take on the role of an individual taxation adviser and independent confirmation should be obtained before acting or refraining from acting upon the information given. The law and HMRC practice are subject to change. This article is also available as a PDF